GEMS: Estate Taxes and the Lifetime Exemption

For ultra-high-net-worth (UHNW) individuals, estate taxes are a significant consideration in wealth preservation and intergenerational planning. In the United States, estate taxes are levied on the transfer of wealth upon death. The federal government imposes this tax on estates that exceed a specified exemption threshold. This paper explains how estate taxes work, outlines the current lifetime exemption rules, and highlights what we believe are key planning considerations.

Understanding Estate Taxes

The federal estate tax applies to the total fair market value of an individual’s taxable estate at the time of death. This includes cash, investments, real estate, business interests, valuable personal property, and other assets. However, only estates exceeding a certain threshold – known as the lifetime exemption – are subject to estate tax. In 2025, the lifetime exemption is set at $13.99 million per individual or $27.98 million for married couples. Assets exceeding this exemption amount are taxed at a 40% federal estate tax rate.

As an example, consider a single individual with a $50 million estate. Upon passing, the first $13.99 million is exempt from federal estate taxes and passes to heirs tax-free. The remaining $36.01 million is subject to a 40% estate tax, resulting in a $14.4 million tax bill. This leaves $35.6 million for the heirs after taxes.

The Unified Credit: Estate and Gift Taxes

The lifetime exemption is unified and applies to both estate and gift taxes, meaning any portion used for lifetime gifts reduces the exemption available at death. For instance, if an individual gifts $5 million during their lifetime, then at the time of their passing, the remaining estate tax exemption would be $8.99 million, rather than the full $13.99 million.

This unified exemption allows individuals to transfer appreciating assets out of their estate during their lifetime, effectively locking in the historically high exemption before it is scheduled to decrease in 2026. Further details on the potential reduction will be discussed later in this paper.

The U.S. tax code provides additional provisions for married couples:

- Unlimited Marital Deduction: Transfers between spouses are tax-free, allowing for an unlimited amount to be passed to a surviving spouse without estate tax consequences. However, this unlimited deduction applies only to spouses who are U.S. citizens. For non-citizen spouses, special rules apply, including the potential use of a Qualified Domestic Trust (QDOT) to defer estate taxes.

- Portability of the Lifetime Exemption: If a spouse dies without fully utilizing their exemption, the unused portion can be transferred to the surviving spouse through an election on the estate tax return (IRS Form 706). This is referred to as the Deceased Spousal Unused Exclusion Amount (DSUEA). For example, if a husband dies in 2025 having used only $12.99 million of his $13.99 million exemption, his surviving wife may claim the remaining $1 million, increasing her exemption to $14.99 million.

State Estate and Inheritance Taxes

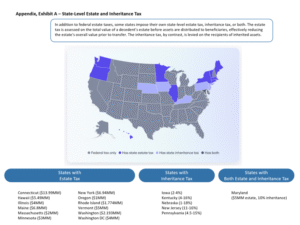

In addition to federal estate taxes, several states impose their own estate or inheritance taxes, often with much lower exemption thresholds. Individuals with significant wealth should incorporate state-level tax considerations into their planning to minimize exposure. For a detailed overview of state-level estate and inheritance taxes, refer to Exhibit A in the Appendix.

Estate Tax Planning: From the Tax Cuts and Jobs Act (TCJA) to the One Big Beautiful Bill Act (OBBBA)

The current estate and gift tax exemption of $13.99 million per person ($27.98 million per couple) was set by the Tax Cuts and Jobs Act (TCJA) in 2017. From the beginning, this expanded exemption was temporary; it was scheduled to sunset at the end of 2025, cutting the exemption roughly in half and reverting to pre-TCJA levels.

This impending reduction prompted many high-net-worth individuals to consider large gifts before the deadline to lock in the higher exemption.

Now, with the passage of the One Big Beautiful Bill Act (OBBBA) in 2025, the landscape has changed. Starting in 2026, the exemption will be $15 million per person ($30 million per couple), indexed annually for inflation. Just as important, OBBBA makes this exemption permanent, eliminating the uncertainty that has often complicated long-term estate planning. This clarity gives families and advisors the ability to plan more thoughtfully, without the pressure of looming legislative changes.¹

5 Common Strategies to Reduce Estate Tax Exposure

Given the magnitude of the federal estate tax (40%), many individuals with significant wealth seek strategies to reduce the size of their taxable estate. By transferring assets during their lifetime – through gifting, irrevocable trusts, charitable donations, and other methods – they can remove assets from their estate while benefiting family members, charitable organizations, or even the individual during their lifetime.

For individuals with estates exceeding the exemption threshold, we believe proactive planning is essential. There are several strategies that can be used to reduce the size of an estate. Some of the most common approaches include:

1. Annual Gift Exclusion

One of the easier strategies to reduce the size of an estate is the annual gift exclusion. As of 2025, individuals can gift up to $19,000 per recipient per year without incurring gift tax or reducing their lifetime exemption. Married couples can combine their exclusions, allowing them to gift $38,000 per recipient. By making annual gifts to children, grandchildren, and other beneficiaries, one can gradually transfer wealth out of their taxable estate.

For instance, a couple with ten beneficiaries could transfer $380,000 per year without using any of their lifetime exemption. By leveraging gifting strategies across multiple years, more substantial reductions in taxable estate value are achievable. A couple who consistently gifts the maximum exclusion to ten beneficiaries over ten years would transfer $3.8 million tax-free.

2. Medical and Educational Exclusion

Direct payments for medical and educational expenses offer another tax-efficient strategy. Payments made directly to the medical provider or educational institution on behalf of someone else are not considered taxable gifts and do not count against the annual or lifetime gift tax exemption. This strategy is particularly useful for helping a loved one cover significant medical expenses or assisting with educational costs. To qualify, payments must be made directly to the provider or institution; reimbursing a beneficiary does not quality.

For example, if an individual wanted to pay his granddaughter’s $60,000 annual tuition, they could pay the university directly and still give her an additional $19,000 tax-free as part of their annual gift exclusion. This strategy reduces their taxable estate and helps preserve their lifetime gift and estate exemption.

3. Charitable Giving

Charitable donations provide a dual benefit: reducing the size of an estate while supporting meaningful causes. We believe charitable gifts, whether made during your lifetime or through a bequest in your will/trust, are an easy way to reduce a taxable estate. Several methods exist, including donor-advised funds, private family foundations, direct donations, charitable remainder trusts (CRTs), charitable lead trusts (CLTs), and qualified charitable distributions (QCDs) from retirement accounts.

4. Irrevocable Trusts

Irrevocable trusts are a cornerstone of estate reduction for UHNW individuals, as assets transferred into these trusts are removed from the taxable estate. We believe this is particularly beneficial because it not only reduces estate tax exposure on the amount transferred, but it also helps to ensure any appreciation of transferred assets is excluded from estate tax calculations. For example, if a person gifts $5 million of stock to an irrevocable trust today, and that stock grows to $10 million over time, the entire $10 million remains outside their taxable estate. Had they kept the stock, the full $10 million would be subject to estate tax.

Various types of irrevocable trusts exist to serve different purposes. Some examples include SLATs (Spousal Lifetime Access Trust), GRATs (Grantor Retained Annuity Trust), ILITs (Irrevocable Life Insurance Trust), and Dynasty Trusts (which are sometimes referred to as Generation Skipping Trusts). These are a few of the most commonly used methods designed to achieve specific tax benefits and estate planning goals.

Many of these trusts are set up as grantor trusts, meaning the grantor agrees to pay the income taxes on trust assets. This structure allows the trust to grow without being diminished by tax payments, effectively providing an additional tax-free gift to beneficiaries over time.

Proper structuring of these trusts can result in significant estate tax savings, particularly when used in combination with valuation discounts and other advanced techniques. Interests in closely held businesses or family partnerships may qualify for valuation discounts due to lack of marketability, liquidity, and/or control, effectively reducing the taxable value of transferred assets. Additionally, intra-family loans and installment sales to grantor trusts can be powerful tools for shifting wealth in a tax-efficient manner.

5. Spend the Money

While gifting and trust strategies are important, an often-overlooked yet straightforward way to reduce the size of an estate is to simply spend the money. Strategic spending, whether on personal enjoyment, experiences, or other purchases, can provide a way to reduce estate tax exposure while enjoying the benefits of accumulated wealth.

Conclusion

Estate tax planning is essential for UHNW individuals and families who wish to efficiently transfer wealth while minimizing tax exposure. By leveraging strategies such as gifting, trust planning, charitable giving, and other more advanced methods, individuals can significantly reduce estate tax liabilities and ensure their wealth is used in ways that align with their financial and personal goals. With estate laws subject to change and the exemption set to decrease, working with experienced estate attorneys, investment advisors, and tax professionals is critical to achieving optimal outcomes for both the individual and their heirs.

Appendix: Exhibit A

Appendix Source: https://www.justvanilla.com/blog/state-level-estate-planning-laws-you-should-know

Sources and Important Disclosures:

¹Source: https://www.justvanilla.com/blog/estate-planning-under-the-big-beautiful-bill. This paper is based on guidance provided in IRS Publication 559: Survivors, Executors, and Administrators. To learn more, you can access the full publication at https://www.irs.gov/forms-pubs/about-publication-559. This material is provided as a service to you by GenTrust, LLC (“GenTrust”) and is distributed for informational purposes only. The information contained herein is not intended to provide investment, legal, tax or accounting advice. GenTrust does not provide legal, tax or accounting advice. Any statement contained in this material concerning tax matters is not intended or written to be used for the purpose of avoiding penalties imposed on relevant taxpayers. Information contained herein is based on third party sources and, although believed to be reliable, has not been independently verified and its accuracy or completeness cannot be guaranteed and is subject to change without notice. Additional information related to GenTrust, can be viewed via GentTrust’s Form ADV Part 2A, which is available at www.adviserinfo.sec.gov. No part of this material may be reproduced in any form, or referred to in any publication, without the express written permission of GenTrust. © 2025 GenTrust. All Rights Reserved.